Bitcoin mining is the storage and exchange of coins. This process helps solve the unique problems that digital currencies present. For example, a $5 bill cannot be issued multiple times, nor can the same amount of money be debited from an account indefinitely. Also, you can't withdraw any more money than what your bank records say. Bitcoin mining is essential for the exchange of currency. However, it does not come without costs. This article outlines the costs, problems, and rewards of bitcoin mining.

Costs of bitcoin mining

Mining bitcoin can be a very lucrative business. However, electricity costs, hardware and electricity usage can all be quite high. Since Bitcoin mining involves specialized computers and hardware, it is necessary to purchase the appropriate amount of electricity. Decentralization makes it even more costly. This also explains why electricity costs are so high. To survive in the Bitcoin mining enterprise, you must have the funds to finance it.

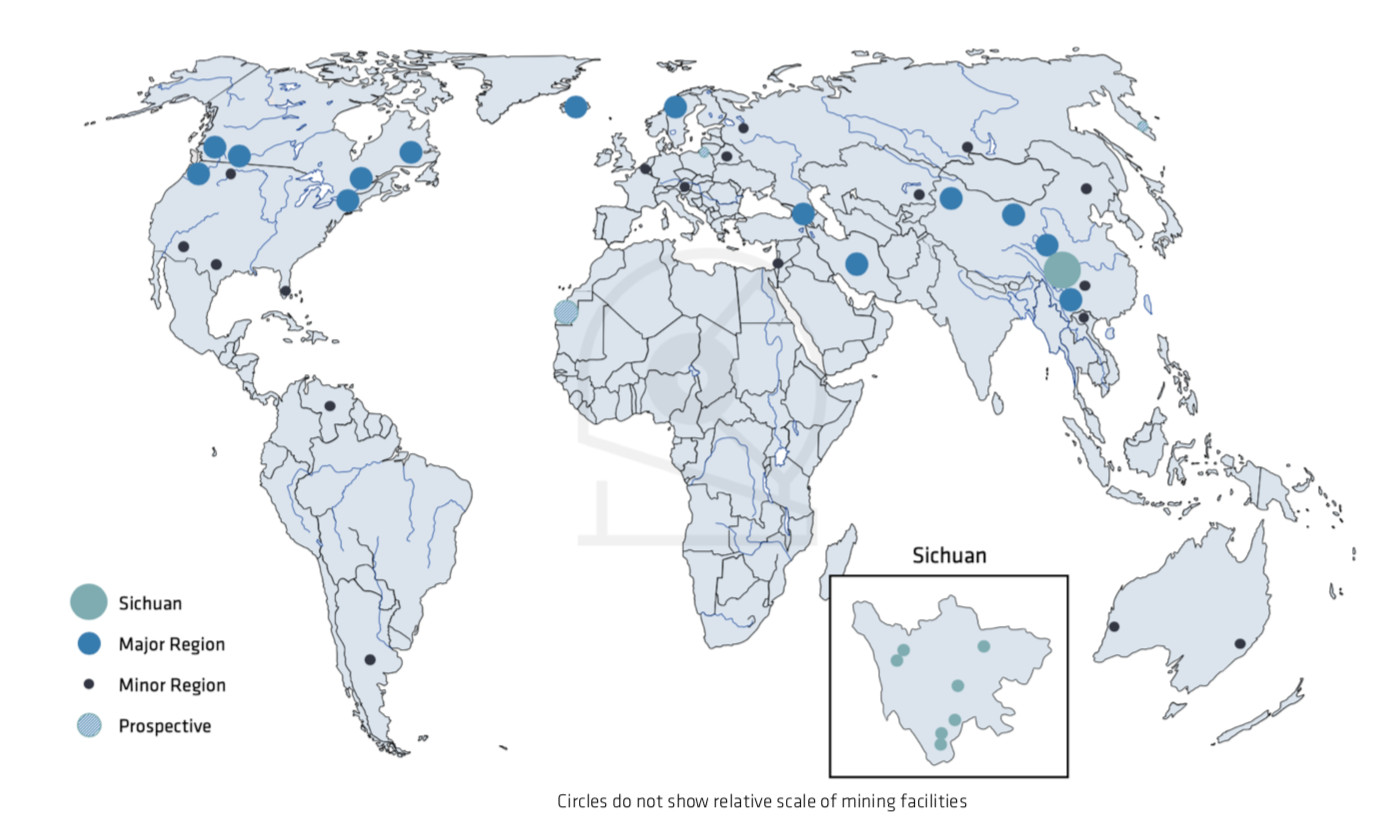

According to the International Energy Agency in 2017, the Bitcoin network consumed 30 Terawatt-hours of electricity. However, it now consumes more that twice as much, between 78 and 101TWh per hour. Each Bitcoin transaction is estimated to produce approximately 300 kilograms of carbon dioxide. This is equivalent to seventy-five millions credit cards swiped. Bitcoin mining would consume the same amount of energy as Austria and Bangladesh. Since most mining facilities use coal-based power, the overall energy consumption of Bitcoin mining is likely to be higher.

Bitcoin mining problems

Bitcoin mining comes with a lot of challenges. This increases the carbon footprint for the world's electricity supply. China is the largest country for Bitcoin mining, and their carbon emissions are alarming. Chinese Bitcoin mining will produce 130 million metric tons carbon emissions by 2024. These concerns aside, Bitcoin mining is worth looking into as an investment. It has other positive impacts on nature.

Digital records such as bitcoins are subject to double-spending or counterfeiting and can be copied. This is why mining is essential. Hacking the bitcoin network can be very expensive so many miners use dedicated networks that reduce external dependencies. However, once a miner is disconnected, syncing transactions may become complicated and more time-consuming. This is especially true if you are mining in remote areas where connectivity is not always reliable.

Bitcoin miners receive rewards

Bitcoin miners generate revenue by verifying transactions. They are awarded blocks of different value as a reward. The amount of block rewards varies depending upon network congestion and transaction sizes. Although the initial rewards for mining bitcoins was high, they decreased as the currency became more expensive. In the past, they would receive a reward of 50 bitcoins for confirming a block, but this changed to only ten bitcoins in 2012, and then a half-billion-bitcoin-block in 2020. However, the current estimate to mine the final bitcoin is February 2140.

However, this recent halving has led to a lot of optimism about the Bitcoin upgrade. It reminds me of the excitement over previous block reward reductions. Even though bitcoin prices plunged by half in July it rallied because of high demand and slower issuance. Dogecoin (which is based upon Bitcoin) rose by more than 1% within 24 hours. Other cryptocurrencies have also been increasing in value. The profits of crypto investors last week were worth $2.09 trillion.

Bitcoin mining uses blockchain technology

Bitcoin mining requires a lot of resources. It verifies transactions and adds them to a ledger. To receive bitcoins, the user must solve complicated mathematical problems. The successful miner will be rewarded with a set amount of these currencies. While blockchain technology isn't a cryptocurrency, it does help solve a subset of bitcoin-related problems. Here are some benefits of blockchain technology for bitcoin mining.

The blockchain is distributed between multiple nodes. Each node is responsible to maintain a copy. Every member of the network must approve any changes to a ledger before they can be added or removed from the blockchain. This method is decentralized and makes it difficult to alter the information and make it ineffective. Blockchains can be transparent because each participant has a unique alphanumeric ID number.

FAQ

Ethereum: Can Anyone Use It?

Ethereum can be used by anyone. However, only individuals with permission to create smart contracts can use it. Smart contracts are computer programs which execute automatically when certain conditions exist. These contracts allow two parties negotiate terms without the need to have a mediator.

Are There any regulations for cryptocurrency exchanges

Yes, there are regulations on cryptocurrency exchanges. Although licensing is required for most countries, it varies by country. A license is required if you reside in the United States of America, Canada, Japan China, South Korea or Singapore.

Which crypto to buy today?

Today I recommend Bitcoin Cash (BCH) as a purchase. BCH has been steadily growing since December 2017, when it was trading at $400 per coin. The price of BCH has increased from $200 up to $1,000 in less that two months. This shows how confident people are about the future of cryptocurrency. It also shows that there are many investors who believe that this technology will be used by everyone and not just for speculation.

How Are Transactions Recorded In The Blockchain?

Each block has a timestamp and links to previous blocks. A transaction is added into the next block when it occurs. This process continues till the last block is created. The blockchain then becomes immutable.

Statistics

- As Bitcoin has seen as much as a 100 million% ROI over the last several years, and it has beat out all other assets, including gold, stocks, and oil, in year-to-date returns suggests that it is worth it. (primexbt.com)

- “It could be 1% to 5%, it could be 10%,” he says. (forbes.com)

- Ethereum estimates its energy usage will decrease by 99.95% once it closes “the final chapter of proof of work on Ethereum.” (forbes.com)

- For example, you may have to pay 5% of the transaction amount when you make a cash advance. (forbes.com)

- This is on top of any fees that your crypto exchange or brokerage may charge; these can run up to 5% themselves, meaning you might lose 10% of your crypto purchase to fees. (forbes.com)

External Links

How To

How to convert Crypto into USD

Also, it is important that you find the best deal because there are many exchanges. You should not purchase from unregulated exchanges, such as LocalBitcoins.com. Do your research and only buy from reputable sites.

If you're looking to sell your cryptocurrency, you'll want to consider using a site like BitBargain.com which allows you to list all of your coins at once. By doing this, you can see how much other people want to buy them.

Once you've found a buyer, you'll want to send them the correct amount of bitcoin (or other cryptocurrencies) and wait until they confirm payment. You'll get your funds immediately after they confirm payment.